Making Rates Great Again

“If I don’t get there one way, I’m going to get to Pennsylvania Avenue another,” Trump jokingly said at the First Presidential debate, referring to the fact that he could always stay at his new 5-star luxury Trump Hotel only four blocks away from the White House if he lost his presidential bid. Ironically, the property tycoon, with a reputation for “shooting his mouth off”, had little to say about real estate during his campaign trail. Yet, how will the Australian real estate market be impacted by Donald Trump’s epic ascension to the presidency?

Many real estate pundits have described the potential impact of a Trump presidency on property markets as uncertain. It is no secret that the President-elect’s policies on trade, financial regulation and fiscal expenditure can adeptly be summarised as “lacking detail”. To further muddy the waters, Trump has shown a tendency to backflip on campaign promises and slogans. Unsurprisingly, these factors have created a sense of anxiousness in the investor community. This anxiety was evident in the roller coaster ride experienced by the global equity markets in the hours after voting closed. Thankfully, the markets recovered on the back of Trump’s acceptance speech when he announced those special words “infrastructure spending”.

Although many of Trump’s campaign promises won’t necessarily pass through both chambers of Congress to become law (at least without these policies being watered-down), they are indicative of what Trump intends to achieve. Ramped up fiscal expenditure and tax breaks are a cornerstone of Trump’s playbook – both policies are designed to stimulate domestic demand and stir inflation.

Trump intends to rebuild the nation’s infrastructure. The Trump plan envisages up to a trillion dollars worth of infrastructure investment over a 10-year period. Furthermore, the San Francisco Fed has reported that the typical fiscal multiplier for infrastructure spending can be anywhere between 0.5 to 1.5x. Increased spending on infrastructure will place a heavy demand on the construction industry, driving employment, presumably creating millions of jobs, and turbo charging America’s GDP growth.

Under the guise of “fighting for free trade” the President-elect intends to renegotiate the NAFTA agreement, label China a currency manipulator and repudiate the Transpacific Trade Partnership. The IMF has warned that the potential shock from a worldwide increase in tariff and non-tariff barriers (aka protectionism) could result in import price increases by up to 10 per cent over the next three year period.

In addition to the protectionist measures, Trump also plans to reform the taxation system for both individuals and corporations. In order to stop companies moving out of the country because of tax rationales, and to encourage multinationals to repatriate trillions of dollars of foreign profits, the President-elect proposes to reduce the business tax rate from 35 per cent to 15 per cent. The Tax Policy Centre report has forecast that Trump’s tax plan would reduce federal revenues by $6.2 trillion over the next decade, with nearly half of the tax cuts going to the top one percent of households by income. The impact to the US deficit, which would increase by $7.2 trillion (according to the Tax Policy Centre), would result in a Treasuries sell off, higher interest rates and stronger inflation.

For Australian real estate, Trump’s policies have various implications. We have already established that Trump’s policies will accelerate inflation to a much higher rate than was previously anticipated.

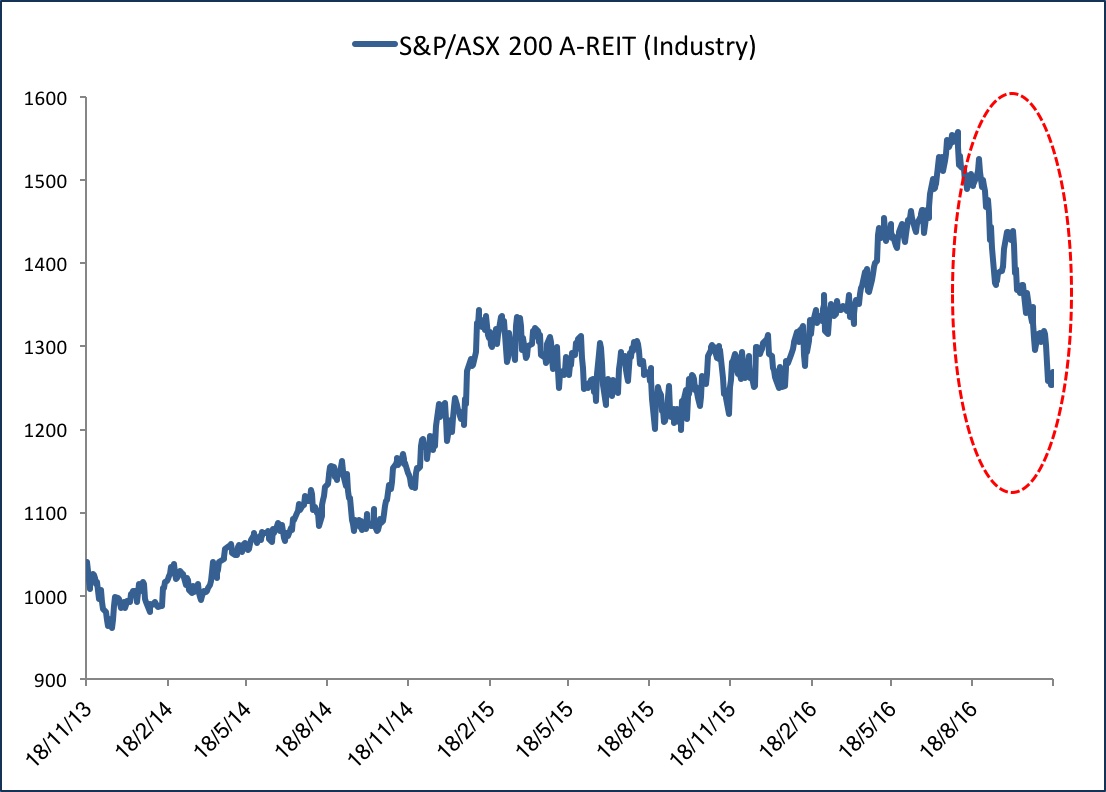

Higher inflation will be particularly harmful to Australia’s real estate investment trusts, which have benefited from the low interest rate environment in recent years. REITs typically offer higher yields than other stocks, however, given an anticipated steeper upward sloping yield curve, REITS will be negatively exposed. To quote Matthew Barasch of RBC, “In a rising interest rate environment, we believe virtually no REIT share price will be spared.” It should be noted that since 1 August 2016, A-REITS have already corrected some 17 per cent.

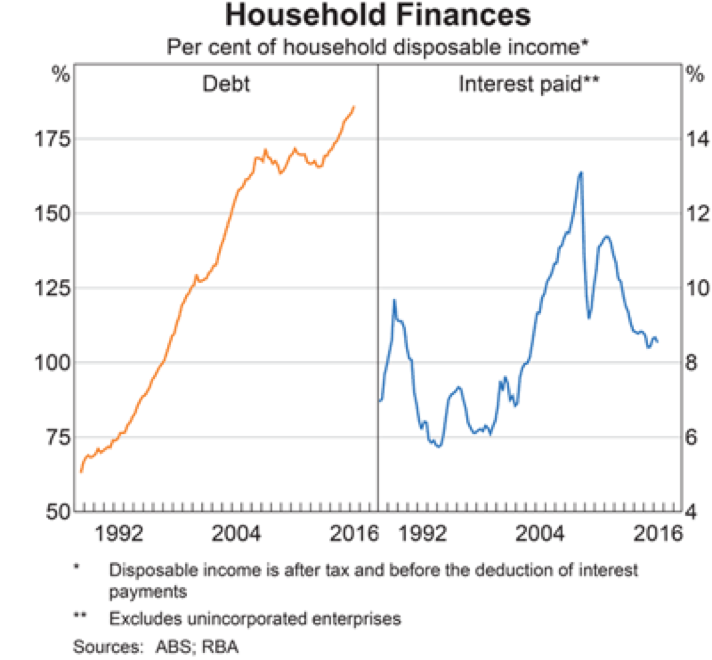

For tangible real estate, there is generally an 18 to 24 month lag between higher bond yields and capitalisation rates, which feed through to real estate values. By way of reminder, real estate values are a function of net operating income divided by the cap rate. 10 year bonds are an excellent predictor of the future direction of real estate cap rates. The 10 year bond rates have increased by almost 0.5 per cent following the US elections. The pace of the Fed rate hike cycle, which is now expected to accelerate, will, in Trident Real Estate Capital’s opinion, force the Reserve Bank of Australia (RBA) to lift rates at greater speed than it initially anticipated. Higher rates are a cause of much concern. The Australian real estate market is at a mature stage in the cycle. This is reflected in the substantial cap rate compression and existing debt levels on household balance sheets. According to the RBA, household debt is equivalent to 185 per cent of annual household disposable income, a record high and up from around 70 per cent in the early 1990s.

The reason for the increase in debt has been largely the result of the RBA’s complacency in reducing interest rates, resulting in households taking on higher levels of leverage. Lower rates are not, however, an Australian phenomenon but an international one. Many governments have struggled to spur domestic growth and as a result have relied heavily on monetary policy.

In 2017, political risk will further be compounded with the scheduled Dutch, German and French elections. We also expect higher oil prices in the new year as the 14-nation OPEC cartel cooperate on production cuts. These factors will accentuate the risk of higher inflation and a steeper yield curve. The increase in market volatility, particularly as Trump begins to reveal his plans to “make America great again”, will inevitably result in some lenders further reducing the availability of debt capital.

Although the era of low interest rates may finally be coming to an end, Trident Real Estate Capital believes Trump will make a difference. The US congress has been in a fiscal limbo for much of the last 8 years. To quote Sam Zell, “[Now] we’re likely to see a reorientation toward growth and a reduction in the regulatory environment…I think it’s a very positive scenario for the US and the world.”

Latest on Twitter

Our latest research argues Australia's 2026 property tax reforms may unintentionally:

• Weaken rentvesting

• Reduce apartment pre-sales

• Lower development feasibility

The result?

Read the research:

#Property #RealEstate #Housing #Development

Everyone’s watching interest rates. Fewer are watching trade policy.

US tariffs are reshaping construction costs, housing supply and rental yields across Australia — and splitting the market in two.

This isn’t cyclical. It’s structural.

https://shar.es/agEdkW

#AustralianProperty

Behind the Server: A Contrarian View on Data Centre Investment | Trident Real Estate CapitalTrident Real Estate Capital http://bit.ly/41DVYlN #DataCenters #RealEstateInvestment #TechInfrastructure #CommercialProperty #ContrarianInvesting #PropTech